BSP’s Interest Rate Primer: Low Rates Are the Cause of Inflation! BSP Rate Hikes: Peso, Treasuries, and Stocks Plunge

It's a supply-side problem, officials say. But they also admit, behind the scenes, it is an issue of money. Nonetheless, domestic financial markets discount the BSP's latest rate hikes.

Neither have capital or capital goods in themselves the power to raise the productivity of natural resources and of human labor. Only if the fruits of saving are wisely employed or invested, do they increase the output per unit of the input of natural resources and of labor. If this is not the case, they are dissipated or wasted—Ludwig von Mises

In this issue

BSP’s Interest Rate Primer: Low Rates Are the Cause of Inflation! BSP Rate Hikes: Peso, Treasuries, and Stocks Plunge

I. Surprise! BSP’s Interest Rate Primer: Extended Low Interest Rates Are the Cause of Inflation!

II. BSP Hikes Ignored: Most Treasury Yields Surge

III. BSP Hikes Ignored: USD Peso Soared to Fresh All-Time Highs!

IV. PSEi 30 Plummets to July Lows as Stagflationary Forces Spreads!

BSP’s Interest Rate Primer: Low Rates Are the Cause of Inflation! BSP Rate Hikes: Peso, Treasuries and Stocks Plunge

I. Surprise! BSP’s Interest Rate Primer: Extended Low Interest Rates Are the Cause of Inflation!

Figure 1

Surprise!

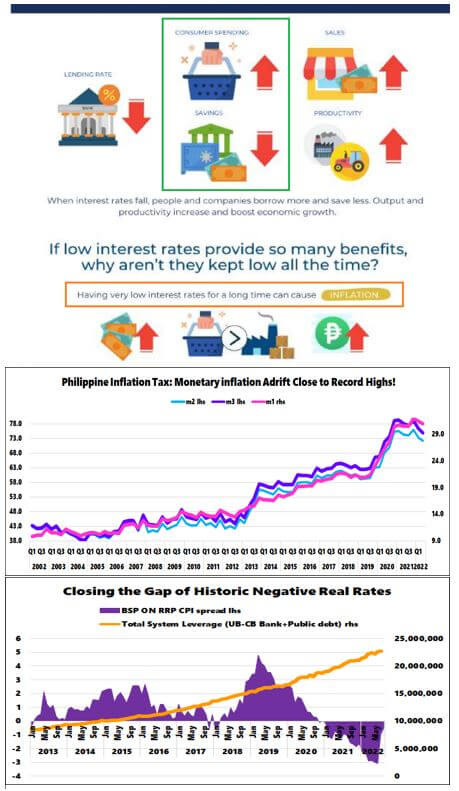

The BSP has an important revelation. In their primer of "Why Should Interest Interest You," they actually state that Having very low interest rates for a long time can cause INFLATION.

(BSP, 2022) [figure 1, topmost pane]

See? The root of inflation is artificially lowered rates!

But the public barely knows of this position by the BSP. This media literature on "financial inclusion and consumer protection" is camouflaged with the avalanche of many other materials.

To begin with, the BSP misattributes money as a "second-round" effect of the recent perturbation from price pressures.

After raising rates by another 50 bps last week, they explained: With less money going around and demand for goods and services diminished, prices are expected to go down. “In deciding to raise the policy rate anew, the Monetary Board noted that price pressures continue to broaden,” Dakila said. “Moreover, second-round effects continue to manifest, with inflation expectations remaining elevated in September following the approved minimum wage and transport fare increases,” he added. (Inquirer, 2022)

No. Supply-side disruptions do raise the prices of certain goods and services. But because of the scarcity of purchasing power of individuals, prices of other goods and services should fall; in the condition that the money supply is stable and markets are allowed to clear. But that has not been the case. The BSP continues with its thrust to use liquidity to generate GDP. Ergo, too much money chased too few goods.

But here is the thing. For the longest time, the BSP has pursued a "zero-bound rate" strategy as part of its precept of "inflation targeting" for the goal of "price stability." (BSP, 2020)

The pandemic justified the intensification of its use. Policy rates dived to an all-time low of 2%. The BSP mimicked a global central bank trend of policy activism.

Yet, their data also reveals that while money supply growth has trended higher over the years, it exploded from Q4 2019 to a new milestone in 2021 and has hovered around this area.

The increase in the money supply relative to the GDP tell us that the BSP imposed on the economy the zero-bound policy to promote "financialization." Or it used monetary policy and liquidity measures to advance the interests of the government and the banking and financial industry through the acceleration of credit expansion.

The GDP is now entirely dependent on the sustained growth of the money supply.

The Keynesian ideology of attaining economic utopia from unfettered spending is the foundation for such policies.

Because such policy ignores the ramifications of the distribution of resource allocation, the importance of time, opportunity costs, balance sheet conditions, and the function of the entrepreneur, the backlash from it emerges over time.

Or, its effects are asymmetric and intertemporal. The distribution benefits some segments, but most don't. And the consequences occur across time or are time-lagged from their imposition.

For instance, the initial phase of such measures triggers a boom. Because of this, the public embraces the easy money policy as "sustainable," which they attribute to the "competence" of the central bank.

The problem is: Imbalances from such policies accrue, such that once it reaches a tipping point, disorderly adjustments are the consequences.

Today's problems are the manifestations of the excesses of interventionist policies.

The evidence is everywhere.

And as pointed out last week, the diffusion of liquidity from election spending and increases in consumer leveraging in the banking system resulted in a pronounced boost in food retailers' sales in the 1H 2022.

Meanwhile, the non-food retail sector exhibited modest improvements.

In any case, the boost in demand, which may reflect price hikes more than volume, signified a first-order effect.

But authorities would not permit the public to know this. Instead, they passed the blame onto the supply side. They hope to sustain their unsustainable model of a GDP driven by public spending financed by debt and the inflation tax. It likewise hopes that the credit-dependent bubble sectors complement its agenda.

At any rate, the latest increase in policy rates has barely alleviated the apprehensions of the domestic financial markets.

Nevertheless, the consensus experts have, in near unanimity, laid the burden on the US Federal Reserve.

II. BSP Hikes Ignored: Most Treasury Yields Surge

Figure 2

Technically, the BSP narrowed the difference between its policy rate (4.25%) and the official CPI (6.3%). But its spread remains "negative," coming off its milestone gap. (Figure 1, lowest pane)

The official CPI should not be seen as static (even as political agenda seems to dictate its calculations).

In this regard, the domestic financial markets respond to it.

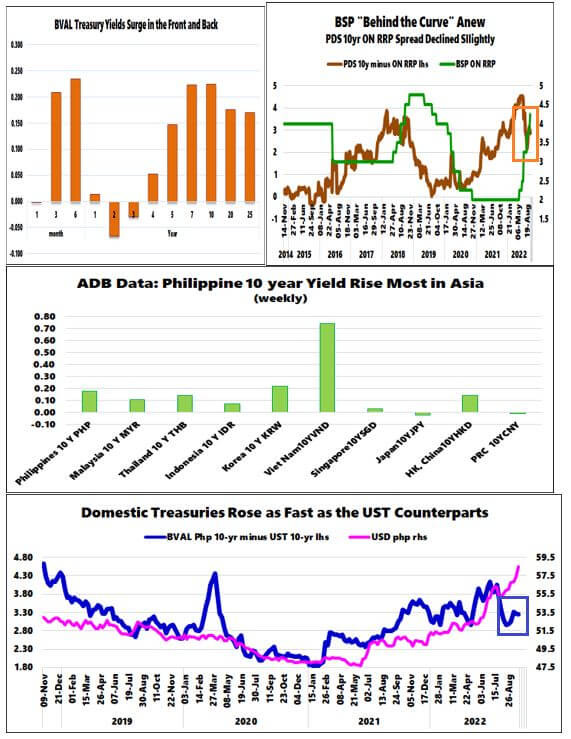

Last week's hike seems to have been ignored by institutional treasury traders. Most of the T-Bills and T-Bonds yields soared this week. (Figure 2, left topmost pane)

With traders seemingly unconvinced, the 10-year and BSP ON RRP (official rate) spread barely came down. (Figure 2, right topmost window)

In Asia, the yield of the 10-year Philippine Treasury was the third fastest gainer after Vietnam and South Korea. (Figure 1, middle pane)

And while its spread against the UST counterpart was almost unchanged from last week. The local bond yields have risen faster than its UST peer since 2021.

The faster yield increase in domestic treasuries is a problem of the US Fed?

III. BSP Hikes Ignored: USD Peso Soared to Fresh All-Time Highs!

Figure 3

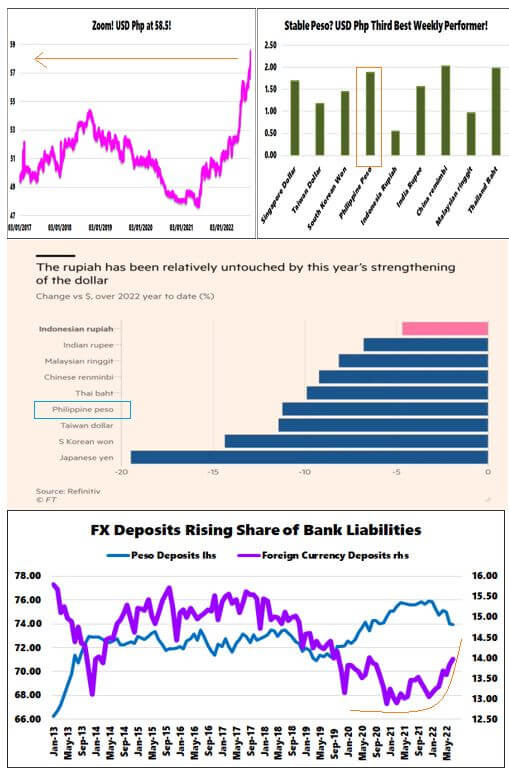

Once again, the USD Php closed the week at 58.5 a fresh high. (Figure 3, left topmost window)

Like their treasury peers, currency traders likewise glossed over the move of the BSP.

Suddenly, the consensus experts have been piling upon each other to "forecast" the USD at Php 60 and above. They are the experts of momentum. They chase a trend in fashion.

A bank commented that investors have started to rotate out of the peso and into USD financial products. But this is to be expected. The FX deposits share of bank liabilities has dramatically risen since Q1 2021. However, they seem to have noticed it only now. (Figure 3, lowest pane)

The USD-Peso was this week's third-best performer after the USD-Yuan and the Thai baht.

Sure, authorities label the USD Php as "middle of the pack," but that would be comparing the problems of advanced economies, likewise suffering from the backlash of heavy indebtedness.

But if this is true, why has the Indonesian rupiah been the outlier? What has made the rupiah seemingly immune to the "strong dollar" problem?

Such "appeal to the majority" rationalizations constitute the sentiment of the consensus, who never saw this coming.

We have argued way back that the Other Reserve Assets (ORA), or derivatives and public borrowings that comprised the record buildup of the GIR, thereby signified the "USD shorts."

Since these borrowings require repayments, are these reserves not only artificial and temporary but represent USD shorts? That is, shorts as in “the mismatch (maturity) between short-term interbank borrowing (globally) on the liability side supporting and maintaining longer duration loan or security assets”…

The bigger their USD liabilities, the more prone the BSP is to a squeeze. (Prudent Investor, 2020)

It does not help when authorities use gaslighting to assuage the public from reality.

In all these cases, the problem is never that the dollar is "too strong." The problem is that other central banks are even worse, and that depreciation of other currencies are causing instability, lost wealth, and economic crises. (McMaken, 2022)

IV. PSEi 30 Plummets to July Lows as Stagflationary Forces Spreads!

Figure 4

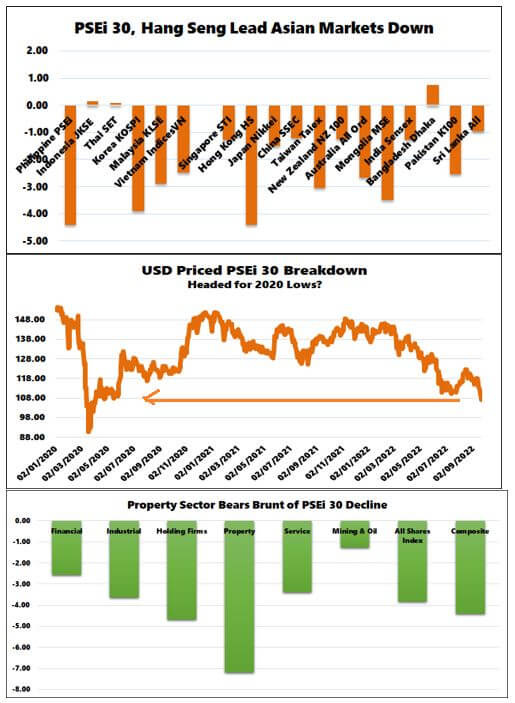

The PSEi 30 tumbled by another 4.42% this week, its fifth weekly decline for an aggregate 8.8% markdown. The PSEi 30 is back at its July levels.

Along with Hong Kong's Hang Seng Index (-4.42%), the PSEi 30 plunge vitiated weekly returns of Asian equities by 1.29%, despite the 11.84% surge of the equity bellwether of Laos.

The PSEi 30 tumbled by another 4.42% this week, its fifth weekly decline for an aggregate 8.8% markdown. The Sy Group skewed the PSEi 30 is back at its July levels.

Interestingly while global banks have taken a thrashing, shares of domestic banks had been least affected (-2.57%), even as its main client, the property sector (-7.18%), bore the brunt of the selldown.

Global equity markets, including the PSEi 30, seem oversold and may be due for a rebound. But in bear markets, oversold markets can remain oversold for an extended period.

As a reminder, we are in an inflationary bear market, an episode not seen since the 70s.

As it is, as stagflationary conditions spread, the risk of something breaking and causing a contagion from the present fragile global and domestic conditions only crescendoes.

Or, the speed of the plunging currencies of China, Japan, and Europe (or the surging USD) makes the world vulnerable to a sudden stop and subsequently, a crisis.

Be careful out there.

___

References:

BSP Media and Research, "Why Should Interest Interest You," (2022) bsp.gov.ph

BSP Media and Research, Inflation Targeting, March 2020 bsp.gov.ph

Inquirer.net, BSP again raises rates by 0.5 ppt to quell stubborn inflation, September 23, 2022

Prudent Investor BSP’s April 2020 FSR: PSE’s Soaring Debt-at-Risk, Bank and Financial Vulnerabilities, Risks of Re-Fitting of the Economy and More… June 28, 2020

McMaken, Ryan, Central Bankers Are Gaslighting Us about the "Strong Dollar", September 20, Mises.org